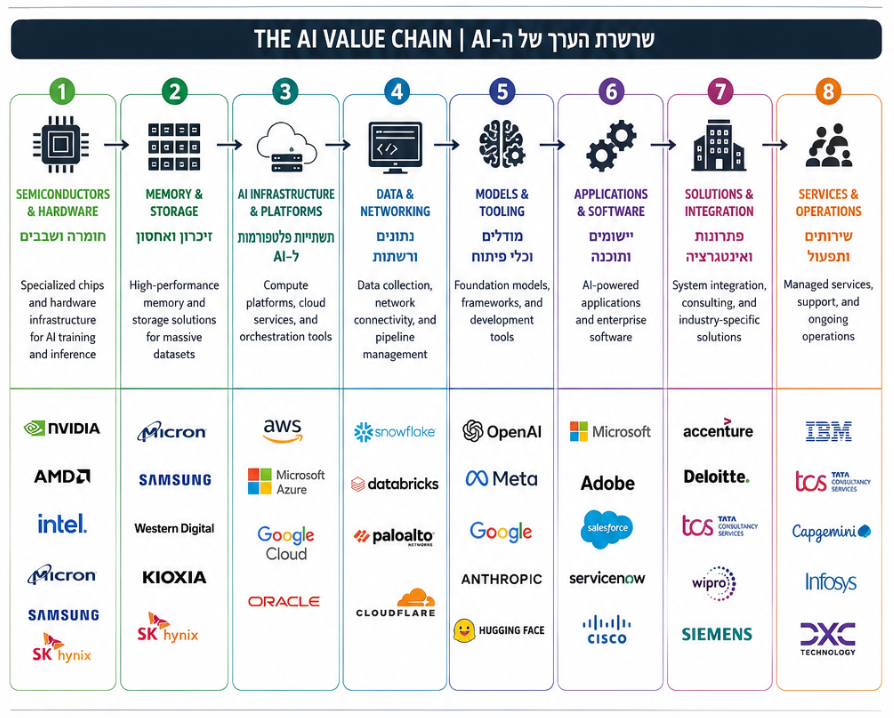

When investors think about artificial intelligence, they usually begin with chipmakers, large language models and cloud platforms. Yet every answer generated on a screen relies on a much broader industrial chain: semiconductor factories, memory chips, servers, optical switches, fiber cables, transformers, generators, cooling systems, real estate, cybersecurity and infrastructure-management software.

AI is therefore not only a technological revolution. It is gradually becoming one of the largest infrastructure investment cycles of the coming decades.

The International Energy Agency expects global data-center electricity consumption to more than double to roughly 945 terawatt-hours by 2030. Consumption is projected to grow by around 15% annually, more than four times faster than electricity demand across the rest of the global economy.

Layer One: The Chips That Perform the Computing

At the center of the value chain are the processors used to train and run AI models.

This layer includes:

GPUs and AI accelerators

Nvidia, AMD and custom accelerators developed by cloud providers.

Semiconductor manufacturing

TSMC, Samsung and Intel, which operate advanced fabrication plants.

Chipmaking equipment

ASML, Applied Materials, Lam Research and KLA supply the machinery required to manufacture advanced semiconductors.

Networking and custom silicon

Broadcom, Marvell and other companies provide networking chips, switches and components connecting thousands of processors.

The economic logic is straightforward: as the number of models, users and applications grows, demand for computing capacity increases. Nvidia reported fiscal 2026 revenue of $215.9 billion, up 65% from the previous year, illustrating the extraordinary scale of the AI infrastructure cycle.

This is also one of the most competitive layers. Cloud providers are developing their own processors, customers are seeking lower-cost alternatives, and technological progress can rapidly shift the balance of power.

Layer Two: Memory, Storage and Advanced Packaging

An AI processor cannot operate efficiently on its own. It requires enormous amounts of high-speed memory, storage and data-transfer capacity.

One of the most important bottlenecks is high-bandwidth memory, or HBM. This memory is placed close to the processor and allows data to be delivered at extremely high speed. SK Hynix, Micron and Samsung are among the leading suppliers.

Storage companies such as Western Digital and Kioxia also participate in this layer.

Advanced packaging has become equally important. Modern AI systems combine processors, memory and communication components inside highly complex packages. As systems become denser, more value is captured by packaging, testing, substrates and interconnect technologies.

Layer Three: Servers and AI Systems

Once chips are manufactured, they must be integrated into complete computing systems.

Dell, Hewlett Packard Enterprise, Lenovo and Supermicro assemble servers containing processors, memory, storage, power supplies and cooling equipment.

This layer can generate large sales volumes, although margins are generally lower than in chip design. Competitive advantages come from supply-chain management, rapid delivery, engineering capability and customer support.

As the market shifts from model training toward widespread commercial inference, demand may expand beyond hyperscale clusters into enterprise servers and on-premise AI systems.

Layer Four: Networking, Optics and Connectivity

An AI data center is not merely a collection of individual computers. It functions as one enormous supercomputer.

Thousands of processors must exchange data at extremely high speed. As a result, internal networking has become a major share of total system cost.

This ecosystem includes:

Arista Networks, Cisco, Juniper and Nvidia in networking

Coherent and Lumentum in optical components

Amphenol, Corning, Belden and Prysmian in connectors, fiber and cabling

As AI models grow, delays in moving data can become as important as processor performance. Bandwidth, latency and optical connectivity are therefore becoming nearly as critical as computing power itself.

For investors, this layer is attractive because demand is not tied to a single processor supplier. Every large computing cluster requires switches, fiber, connectors and optical systems.

Layer Five: Electricity, Backup Power and Grid Infrastructure

AI data centers are becoming industrial-scale electricity consumers.

They require:

Grid connections

Transformers and substations

Uninterruptible power supplies

Backup generators

Electrical switchgear

Power-management equipment

Energy-storage systems

Schneider Electric, Eaton, ABB, Siemens Energy, GE Vernova, Vertiv, Hubbell and Cummins are among the companies active in this layer.

Electricity is becoming a central constraint because in many regions the limiting factor is no longer chip availability, but access to grid capacity. U.S. electricity consumption is expected to reach new records in both 2026 and 2027, partly because of rising demand from AI-oriented data centers.

A company may purchase processors, build a facility and install servers, but without reliable power the system cannot operate.

Layer Six: Cooling and Thermal Management

AI processors consume large amounts of electricity, much of which is converted into heat.

Traditional data centers relied mainly on air cooling. High-density AI systems increasingly require liquid cooling, heat exchangers and precision thermal-management systems.

Companies in this field include Vertiv, Schneider Electric, nVent, Modine, Trane, Carrier, Johnson Controls and Daikin.

Cooling shows how AI spending benefits companies that are not traditionally classified as technology businesses. As power density per server rack rises, cooling becomes an essential system rather than a secondary expense.

Layer Seven: Construction, Engineering and Raw Materials

Before a data center can operate, it must be designed and built.

Projects require steel, copper, aluminum, concrete, electrical systems, cables, engineering services and specialized contractors.

Quanta Services, Jacobs, Fluor and AECOM are involved in engineering and construction. Nucor, Steel Dynamics, Freeport-McMoRan and other material suppliers benefit from demand for construction inputs.

This layer is more cyclical and is sensitive to commodity prices, labor costs, interest rates and project delays. However, once a large building cycle begins, order backlogs can extend for several years.

Layer Eight: Data-Center Real Estate

Data centers require land, power, connectivity, permits and proximity to users and communication networks.

Digital Realty and Equinix are among the most prominent listed real-estate companies in the sector. They operate alongside private infrastructure companies and hyperscalers building their own facilities.

The value of a data-center site is determined by more than the size of the building. Key variables include:

Available electrical capacity

Speed of grid connection

Fiber availability

Expansion potential

Cooling and water costs

Distance from customers and business centers

In some markets, land with access to power has become a strategic asset.

Layer Nine: Cloud, Models and Applications

At the top of the value chain are the companies selling computing services, models and AI applications.

Cloud infrastructure

Microsoft Azure, Amazon Web Services, Google Cloud and Oracle.

Models and platforms

OpenAI, Anthropic, Google, Meta and other developers.

Enterprise applications

Microsoft, Salesforce, ServiceNow, Adobe and Palantir integrate AI into existing products and workflows.

Cybersecurity and monitoring

Palo Alto Networks, CrowdStrike, Datadog and Dynatrace protect and monitor AI environments.

This is where infrastructure investment must eventually translate into revenue. The central question for investors is whether AI-related income will grow fast enough to justify the enormous amount of capital being deployed.

Where Are the Bottlenecks?

The AI value chain does not expand evenly.

At first, the primary shortage was advanced processors. Then HBM memory and advanced packaging became major constraints. Today, bottlenecks are spreading to electricity, transformers, cooling, grid connections, construction labor and project-development timelines.

This is an important lesson for investors: the company with the most famous technology is not always the company with the strongest pricing power. A smaller supplier of electrical equipment, fiber components or cooling systems may sometimes benefit more directly from supply shortages.

How Should Investors Evaluate Companies Across the Chain?

1. Position in the Value Chain

The more critical and difficult a product is to replace, the greater the potential for pricing power and high margins.

2. Exposure to Bottlenecks

Companies operating in supply-constrained markets can experience rapid order growth even when they do not sell a product explicitly labeled as AI.

3. Customer Concentration

Many suppliers depend on a small number of hyperscale customers. A major customer can accelerate growth, but it can also create risk if investment plans are delayed.

4. Return on Invested Capital

Revenue growth alone is not enough. Investors should examine how much capital is required to generate that growth and whether returns justify the investment.

5. Duration of the Investment Cycle

Semiconductor orders may move quickly, while electricity, construction and real-estate projects often extend over several years.

6. Valuation

A great company is not automatically a great investment at any price. When a stock already discounts years of exceptional growth, even strong results may disappoint the market.

The Investment Conclusion

The AI revolution is not simply a race to build the most powerful processor.

It is creating simultaneous demand across semiconductors, memory, networking, electricity, cooling, real estate, construction, cybersecurity and software. The entire chain benefits, but not every company benefits equally or at the same stage.

The first phase was dominated by chip and server suppliers. The next phase expanded into networking, optics and memory. As more data centers are built, attention is now shifting toward power, cooling, substations, construction and data-center real estate.

For investors, the challenge is not merely to identify which companies are associated with AI. The real challenge is to identify the next bottleneck, determine who possesses pricing power, understand who can expand capacity and recognize which stocks are already priced as though growth will continue indefinitely.

Have a take on this?

Jump into the TradeTechAI Discord to discuss this article with other traders.

Written by

Admin User

Editor

Editor at TradeTechAI, covering market analysis, trading strategies, and portfolio insights.