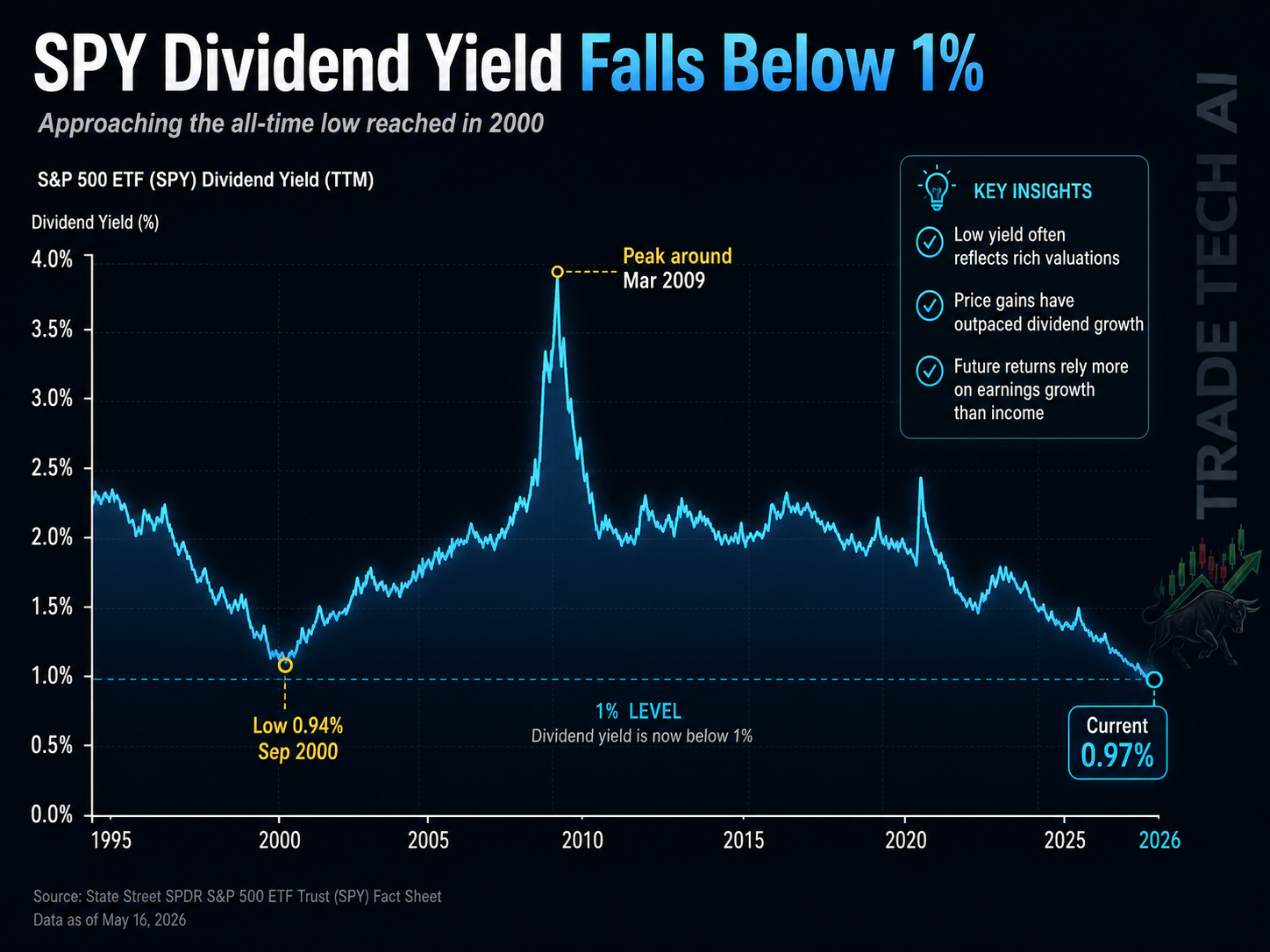

The dividend yield on SPY, one of the world’s most important ETFs tracking the S&P 500, has moved below 1%. The yield is around 0.97%, very close to the historic low seen around the year 2000. Yahoo Finance currently shows SPY’s yield at about 0.98%, placing it near one of the lowest levels in recent decades.

At first glance, this may look like a small technical detail. In reality, it is one of the clearest signals for understanding U.S. equity market valuations. Dividend yield is calculated by comparing the dividends paid by the companies in the index with the price of the index or ETF. When prices rise much faster than dividends, the yield falls. So a very low dividend yield does not only mean companies are paying less. It mainly means investors are willing to pay a very high price for those companies.

The simple implication is that an investor buying the S&P 500 through SPY today receives very little current income from dividends. In the past, dividends were a meaningful part of equity returns. Today, with the yield below 1%, most of the investor’s expected return must come from price appreciation rather than income. In other words, the investor is much more dependent on growth, earnings, optimism and the market’s ability to keep justifying high valuations.

This represents a deep shift in the nature of S&P 500 investing. The index is no longer dominated only by industrials, banks, energy companies and consumer businesses paying relatively high dividends. It has become an index led by giant growth companies, especially in technology, communication services, semiconductors, cloud computing and artificial intelligence. Many of these companies prefer to reinvest profits into growth, research, development and infrastructure, or return capital through share buybacks rather than raising dividends aggressively.

That is where buybacks become important. Over the past few decades, more U.S. companies have returned capital to shareholders through buybacks, not only dividends. A buyback can reduce the number of shares, improve earnings per share and support the stock price, but it does not provide the investor with direct cash income the way a dividend does. So an investor who looks only at dividend yield may miss part of the shareholder-return picture, but an investor who ignores the dividend yield completely may also miss an important valuation signal.

The comparison with the year 2000 is especially interesting. During the dot-com bubble, dividend yields fell to unusually low levels because stock prices, especially technology stocks, rose much faster than earnings and dividends. It is important to be clear: a low dividend yield does not automatically mean the market is in a bubble, and it does not mean the market must fall tomorrow morning. But it does mean that the market is priced with a high degree of optimism and that the margin of safety is smaller.

Today’s market is different from 2000 in several important ways. The largest companies in the index are not just technology dreams with no revenue. Many of them are highly profitable businesses with massive cash flow, powerful competitive advantages and strong balance sheets. On the other hand, their valuations are elevated, expectations are enormous, and a meaningful part of the index’s gains depends on a relatively small group of mega-cap stocks.

That is why a dividend yield below 1% should not be read as an immediate crash signal, but as a warning light. It tells us that the market offers less current income, depends more heavily on price appreciation, and is more sensitive to earnings disappointments, rising bond yields or a shift in sentiment around growth stocks.

For investors, there are several important takeaways. First, anyone looking for current income cannot rely only on the broad S&P 500. They may need to consider quality dividend stocks, dividend ETFs, bonds, money-market funds or a broader asset mix. Second, investors in the broad index should understand that future returns are now more dependent on earnings growth and sustained high valuations, and less on dividends. Third, in this kind of market, selectivity, diversification and risk management become more important.

It is also important to understand the difference between price return and total return. The S&P 500 is usually quoted as a price index, meaning it does not include the impact of dividends. To see the full investment picture, investors should also look at total return indices, which include reinvested dividends.

The bottom line: a dividend yield below 1% on SPY is not an automatic reason to exit the stock market, but it is a clear sign that valuations are high, expectations are elevated, and a large part of future returns depends on continued price appreciation rather than current income. This is a market that can still rise, especially if earnings continue to grow and AI remains a powerful driver. But it is also a market where valuation mistakes can become much more expensive.

Have a take on this?

Jump into the TradeTechAI Discord to discuss this article with other traders.

Written by

Admin User

Editor

Editor at TradeTechAI, covering market analysis, trading strategies, and portfolio insights.